The UAE just walked out on OPEC. The real question is what Saudi Arabia does next.

On Tuesday, the United Arab Emirates announced it would withdraw from OPEC and OPEC+ on 1 May, ending a relationship that began when Abu Dhabi joined the cartel in 1967, four years before the UAE existed as a country. The headlines have focused on the politics — including the UAE's fracturing relationship with Saudi Arabia, the timing during the Iran war and Trump's long-standing complaints about OPEC pricing. All of that matters. But the more interesting story is economic, and it has been building for a decade.

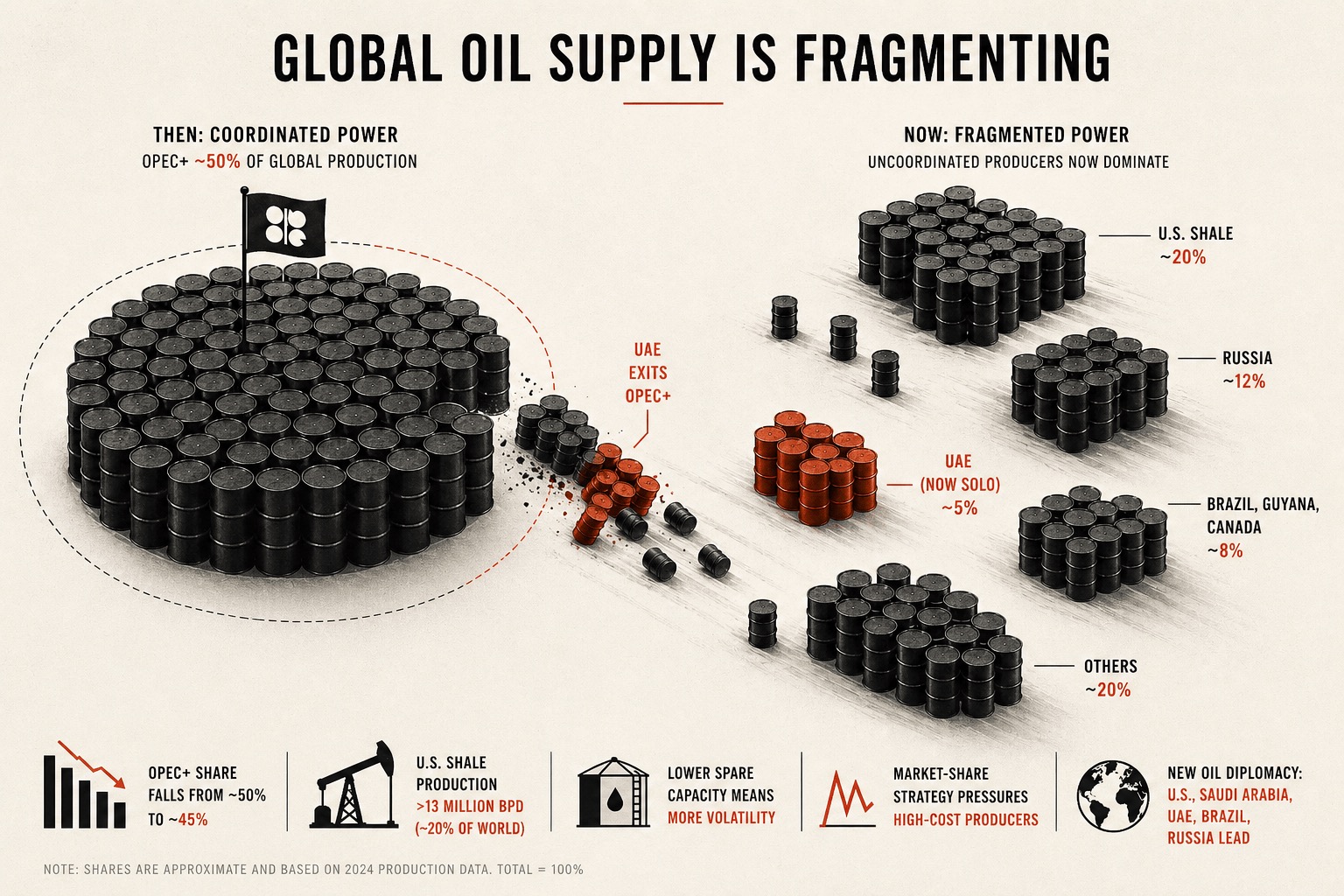

What the UAE actually walked away from

OPEC's basic value proposition to members is straightforward: accept a quota you don't love in exchange for a price floor you couldn't otherwise sustain. The cartel works by holding back collective production — withholding supply to support price — and dividing the resulting pain proportionally among members. When it works, everyone earns more revenue from less oil. When it stops working, members start asking why they are carrying the cost.

The UAE has been asking that question for years. ADNOC has spent around $150bn on a capacity expansion programme that has lifted the country's production capacity by nearly 40% over the last six years to 4.85 million barrels per day, with a target of 5 million by 2027. But its OPEC+ quota held it to 3.4 million. It was, in effect, paying to build infrastructure it wasn't allowed to use — while watching Iraq and Kazakhstan routinely overproduce against their own quotas with little consequence. Energy Minister Suhail Al Mazrouei made the framing explicit: the UAE wants the freedom to act in its national interest, including reaching its 5 million bpd target, and it can no longer do that inside the group.

This isn't a sudden divorce. It is the result of long-running dissatisfaction with quotas, accelerated by a war that gave the UAE both a reason (its export economy is being throttled by Iranian attacks on Hormuz shipping) and a window of cover (the news landed in a market where physical supply is so disrupted that one country's quota status barely registers). But it is also in part the result of a deteriorating relationship with its neighbour Saudi Arabia, prompted by disagreements over the war in Yemen.

Why the price impact is smaller than it looks

The instinctive read on a major producer leaving a price-supporting cartel is more supply, lower prices. That logic isn't wrong, it is just that the extra volume will take time to come on stream. Three things mute the immediate effect.

First, the Strait of Hormuz is closed. Roughly 20 million barrels per day of crude and refined products normally transit through it, and the bypass infrastructure was sized for short disruptions, not month-long shutdowns. The UAE's Habshan-Fujairah pipeline (ADCOP) has a capacity of 1.5–1.8 million bpd and is already running at about 71% utilisation — leaving perhaps 440,000 bpd of headroom, constrained more by Fujairah's port loading capacity than by the pipe itself. Until Hormuz reopens, the UAE physically cannot ship the extra barrels its quota exit theoretically unlocks.

Second, the war has drained inventories. Saxo Bank's commodity strategist has pointed out that the conflict has emptied global commercial and strategic crude stockpiles, leaving the market facing a prolonged rebuilding phase once hostilities end. Extra UAE supply will confront refilling demand. That absorbs the surplus without hammering prices.

Third — and this is the part the UAE is openly leaning into — Al Mazrouei has said the timing was chosen precisely because it would have minimum impact on prices and on fellow producers. Whether you believe that or read it as diplomatic cover for opportunism, the market is treating it as broadly true. The flat reaction to a structural shift of this magnitude tells you the market agrees.

The structural story is more interesting than the price story — for now

OPEC's relevance has been eroding for fifteen years, and the UAE's exit is the latest data point in a longer trend, not an isolated event.

Before this week, OPEC+ — which includes Russia, Azerbaijan, Kazakhstan, Bahrain, Oman and Mexico amongst others — controlled around 41% of global oil production. With the UAE gone, that drops to below 40%. OPEC alone falls to below 25%. US production has climbed to over 13 million bpd — about 20% of the world's oil production — and while OPEC has spent the past decade ceding market share to defend price, non-OPEC countries like Brazil, Guyana, Norway and the US all pump at will. The pool of producers that don't coordinate is now larger, faster-growing, and in some cases lower-cost than the pool that does.

Then look at exits. Qatar left in 2019. Ecuador in 2020. Angola in 2024. Each one was framed as a quota dispute. The UAE is by far the largest, and the first to leave for what it describes as strategic "national interests". Veteran OPEC watcher Gary Ross put it bluntly to Reuters: at the end of the day, Saudi Arabia was essentially OPEC — the only member with serious spare capacity. With the UAE gone, that is even more true. The cartel's price-setting power increasingly rests on one country's willingness to shoulder voluntary cuts alone.

That matters because Saudi Arabia's incentive to keep cutting its production weakens every time someone else benefits without paying. Riyadh has already shown its patience has limits — the abrupt 2024-25 unwinding of voluntary cuts was driven partly by frustration that quota-busters were free-riding on Saudi restraint. The UAE leaving doesn't break that dynamic, but it removes the second-largest disciplined member and leaves the Saudis carrying more of the load alone.

How Saudi Arabia reacts to this departure is going to be very significant for future energy prices. Riyadh now sits inside an increasingly marginalised OPEC alongside Iran — a country with whom it has in effect been at war over the last two months. If its longer-term calculus aligns with what the UAE has decided, the world could quite quickly see dramatically lower oil prices.

What this means for oil production over the next few years

A few things become more likely.

Lower prices. When Hormuz reopens — and it will — the UAE will ramp up production. Rystad Energy predicts that the UAE will act as a normal non-OPEC producer, pumping as much as it can. That equates to about 1.2-1.6 million barrels per day of additional supply entering the market over the next 18-24 months. That's about 1-2% of global demand, which sounds small but, according to their analysis, is enough to shift the price floor downward by $5-15 a barrel in a non-crisis environment. Aside from what the UAE decides to do, the oil market should also see rising production from Venezuela, Mexico, Canada and maybe even Iran and Russia if a permanent peace settlement can be reached in the wars in the Gulf and in Ukraine. All of this additional supply will inevitably lead to structurally lower prices, and that's before any production response from Saudi Arabia, which has the lowest production costs of any oil producing nation at about $10 per barrel.

More volatility, less calibration. One other impact in the oil market that will follow this move, aside from a structurally lower price, is that there is likely to be more price volatility. Spare capacity within OPEC did allow the cartel to manage shocks in the market, and the UAE held a meaningful chunk of that spare capacity. With that gone in a world in which the UAE is maximising output, the global system has fewer shock absorbers, which may mean bigger price swings — but of course, from a much lower base.

Pressure on high-cost producers. Once this extra production comes on stream, and prices adjust down to reflect the structurally oversupplied market, there will be impacts on producers at the other end of the cost curve. Producers which might confront this potential squeeze include those operating in deep water, developments with long payback periods and high-cost oil sands operators. How producers and, importantly, governments react to a structurally lower oil price is going to be very important. The long-term implications of what has happened not just in the Persian Gulf, but what also followed the war in Ukraine, will persist for years to come. Many governments may well conclude that a structural dependence on imported energy creates extreme economic vulnerabilities which can only be mitigated by greater energy independence. This may result not just in greater renewable investment but also in an acceleration of nuclear build, and potentially lower tax burdens on more marginal oil and gas producers to keep production economic. Ultimately the aggregation of some of these decisions could further exaggerate the imbalance between supply and demand, leading to even lower prices and ultimately to more oil demand destruction.

The broader pattern

The UAE leaving OPEC, according to expert analysis, is not the beginning of the end of the cartel. Apparently, that framing overstates it. I am not so sure. The same experts believe that OPEC will continue to exist, that Saudi Arabia will continue to manage prices to the extent that it can, and the remaining members will continue to coordinate. But the OPEC operating model that worked so well in many respects from 1973 to roughly 2014 — a small group of producers with combined market power large enough to set global prices through coordinated supply discipline — has been eroding for over a decade. The US shale boom undermined OPEC's dominant market influence and repeated quota-busting broke its internal discipline. Now the UAE, a major producer with serious underutilised capacity, believes that it can benefit its economy and national interest by leaving the cartel.

Surely the question now confronting a fractured OPEC is can it survive as a price-setting cartel, and will Saudi Arabia still conclude that its national interest is best served by continuing as the only meaningful swing producer? The chances that it decides, like the UAE, that its national interest lies outside of OPEC must now be higher than at any stage in OPEC's 66-year history. If it did decide to follow the UAE's lead, stand by for sustained, much lower oil prices.

The UAE leaves OPEC on Friday, ending nearly 60 years of membership and making it the largest producer ever to walk out of the cartel.

The headlines have focused on the price impact, but for now there isn't one. The Strait of Hormuz is closed, inventories are depleted, and the UAE's bypass infrastructure can't move enough oil to disrupt the market while the war continues. The flat reaction tells you the timing was deliberate.

The real story is structural. OPEC's value proposition — accept a quota you don't love in exchange for a price floor you couldn't otherwise sustain — has been weakening for over a decade. The US shale boom broke OPEC's market dominance. Quota-busting by Iraq and Kazakhstan broke its internal discipline. And now the UAE, having spent $150bn building production capacity it wasn't allowed to use, has shown that for a producer with serious capacity and serious cash, exit is a viable strategic option.

Once Hormuz reopens, the UAE will pump as much as it can — adding 1.2-1.6 million barrels per day to the market over the next 18-24 months. Layer in returning supply from Venezuela, Mexico, Canada and potentially Iran and Russia, and the world is heading for a structurally oversupplied oil market. Prices fall, volatility rises, and the high-cost producers — deepwater, oil sands, long-payback frontier projects — get squeezed.

The bigger question is what Saudi Arabia does. Riyadh has already shown its patience with quota-busters has limits. With the UAE gone, the Saudis are carrying the load of voluntary cuts essentially alone, in a cartel that now also includes Iran — a country it has effectively been at war with for the last two months. If Riyadh decides its national interest aligns with the UAE's, oil prices fall hard and fast. The chances that it reaches that conclusion are higher today than at any point in OPEC's 66-year history. The consensus says OPEC survives this. I'm less convinced.

Related posts

Subscribe to receive Woodford Views in your Inbox

Subscribe for insightful analysis that breaks free from mainstream narratives.