The Housing Minister's Housing Problem

Sometimes, possibly against my better judgment, I read something that is so profoundly stupid and so irritating to me that I have to respond. Today was one such occasion. At the risk of potentially upsetting some readers, I have written about what I read, why I think it’s important and so irritating, and will sprinkle some facts to help inform the issue.

My irritation concerns an article I read last week in the FT (free link), which was given some prominence by this established organ of the mainstream media. The article by Chris Smyth and Julie Steinberg covers the latest proclamations about the new-build housing market from none other than the government’s housing minister, Matthew Pennycook. The minister, who presumably in part “owns” the government’s doomed-to-fail housebuilding target (1.5 million new homes over the life of the parliament – 309,000 delivered since the election), was presumably interviewed by the FT ahead of publishing a new (yawn) housing strategy in the coming weeks.

In the interview, the minister reveals, possibly unsurprisingly, his profound lack of understanding of private enterprise and the issues that govern the supply of new homes. Undeterred by his ignorance, or maybe in complete ignorance of it, the minister ploughs on with his notion that “in the coming weeks (the new strategy) will encourage (whatever this means) alternative business models to those used by large developers, as well as a bigger role for the state.”

Unaware of the hole he has already dug for himself, the minister keeps digging with comments like:

“How we get more volume out of the system is one of the fundamental challenges we face.”

The current housebuilding model “locks in an upward ratchet of land and house prices”, he argued that a better system would make homes more affordable by flattening prices.

This next one is my particular favourite:

If the government’s target of building 1.5 million homes by the end of the parliament is hit and such levels of housebuilding are sustained, “we will be looking at the levelling out of prices and then over the real medium- to long-term perhaps their gradual reduction,” he said.

And finally:

Government was finishing “the bulk of the supply-side measures” and would now focus on ensuring the industry stepped up building.

I am struggling to know where to start, but have decided, as I usually do, to address this issue with some facts, best represented in some charts and brief commentary. Just before I do, however, it should be blindingly obvious to this career mandarin that the housing market, both new build and previously owned, is of profound importance to the health and vibrancy of the UK economy. Unfortunately, what this housing minister seems not to understand is that it is daft government policies, punitive taxation and excessive regulation that have undermined it rather than some kind of flawed housebuilding business model.

So, to the facts:

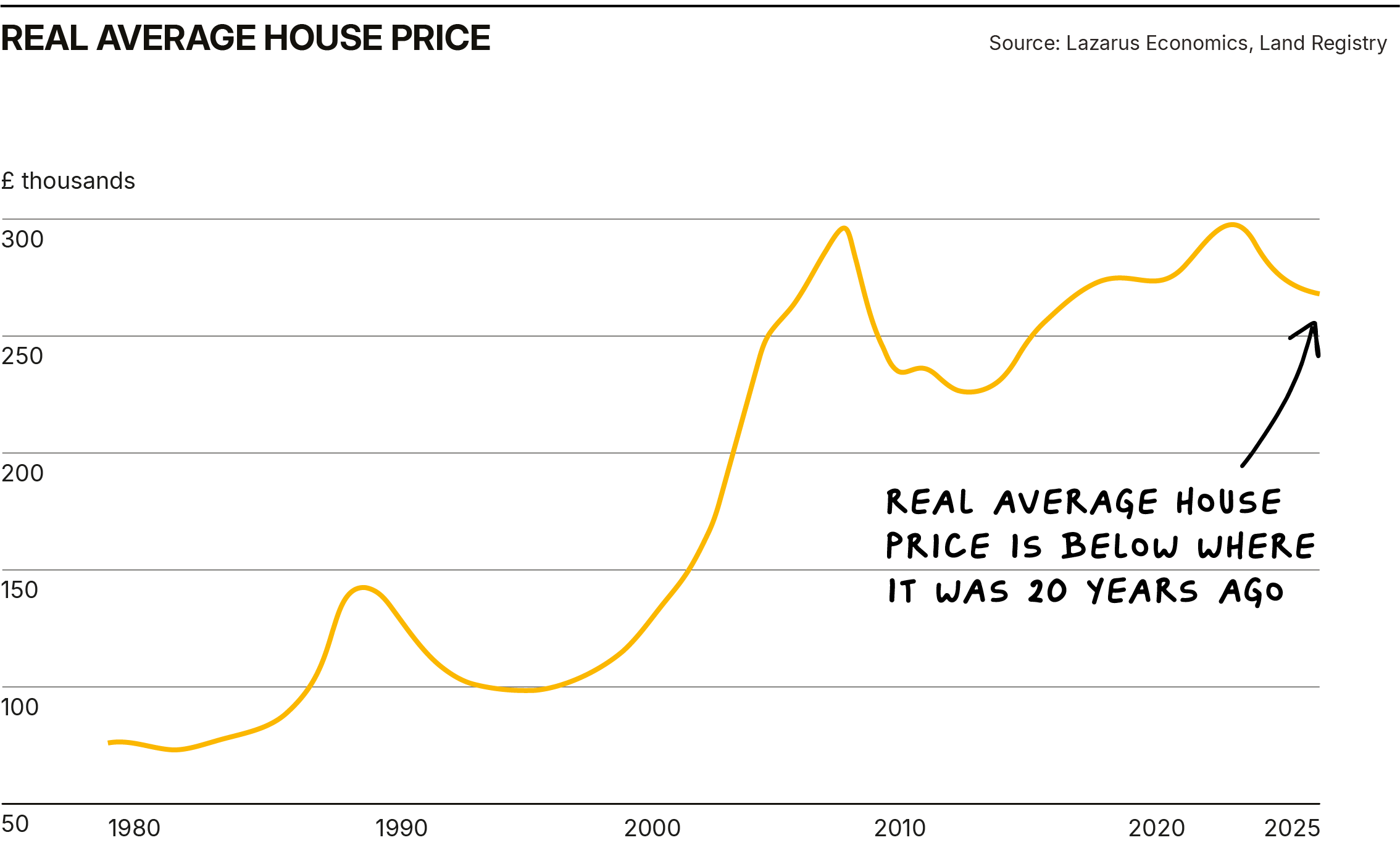

1. Price is not the issue constraining the housing market. In fact, you could argue that the housing market is profoundly depressed, given that in real terms, the average house price is now below where it was twenty years ago.

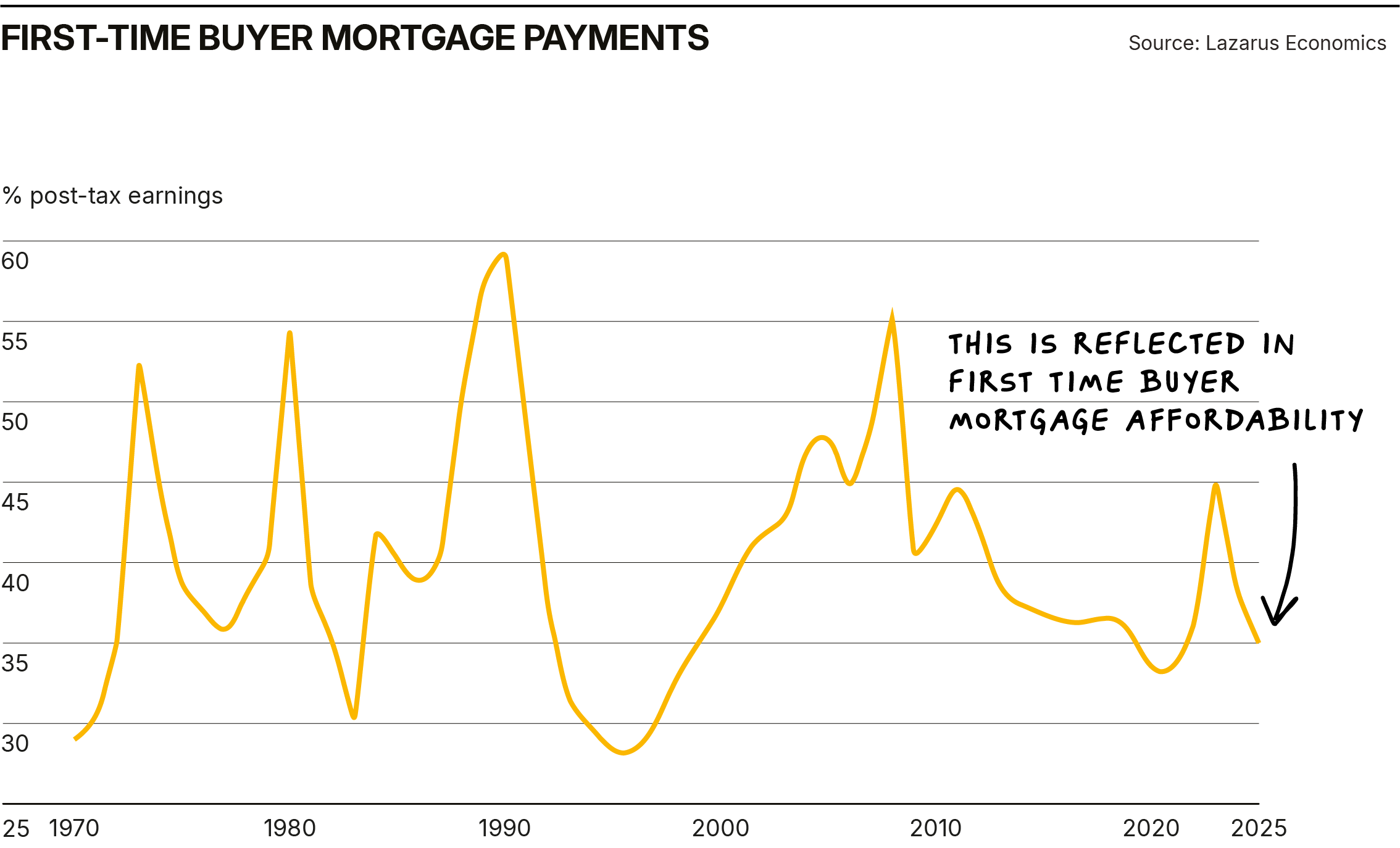

2. And this is reflected in the affordability of first-time buyer mortgage payments – something the minister should be interested in but is seemingly oblivious to, even at current, relatively elevated interest rates.

3. The LSE- and Oxford-educated minister, who has worked only in the public sector, also seems oblivious to the fundamental laws of supply and demand in the housing market. What he fails to understand is that more houses get built when prices are rising, and for very obvious reasons, fewer are built when prices are falling. Quite how the minister is going to persuade private sector housebuilders to abandon this basic mantra is beyond me.

But it gets worse. Later in the piece, the minister criticises the return-on-capital model used by volume housebuilders, suggesting it should be replaced with a volume-based model. (Seemingly unaware that turnover is vanity, profit is sanity.) Disappointingly, the mumbo jumbo continues, with statements like “the state will lean in to diversify the way housing is delivered” and “more SMEs back in the game producing homes at scale, councils building again at scale… and the state doing its part on larger sites in particular.”

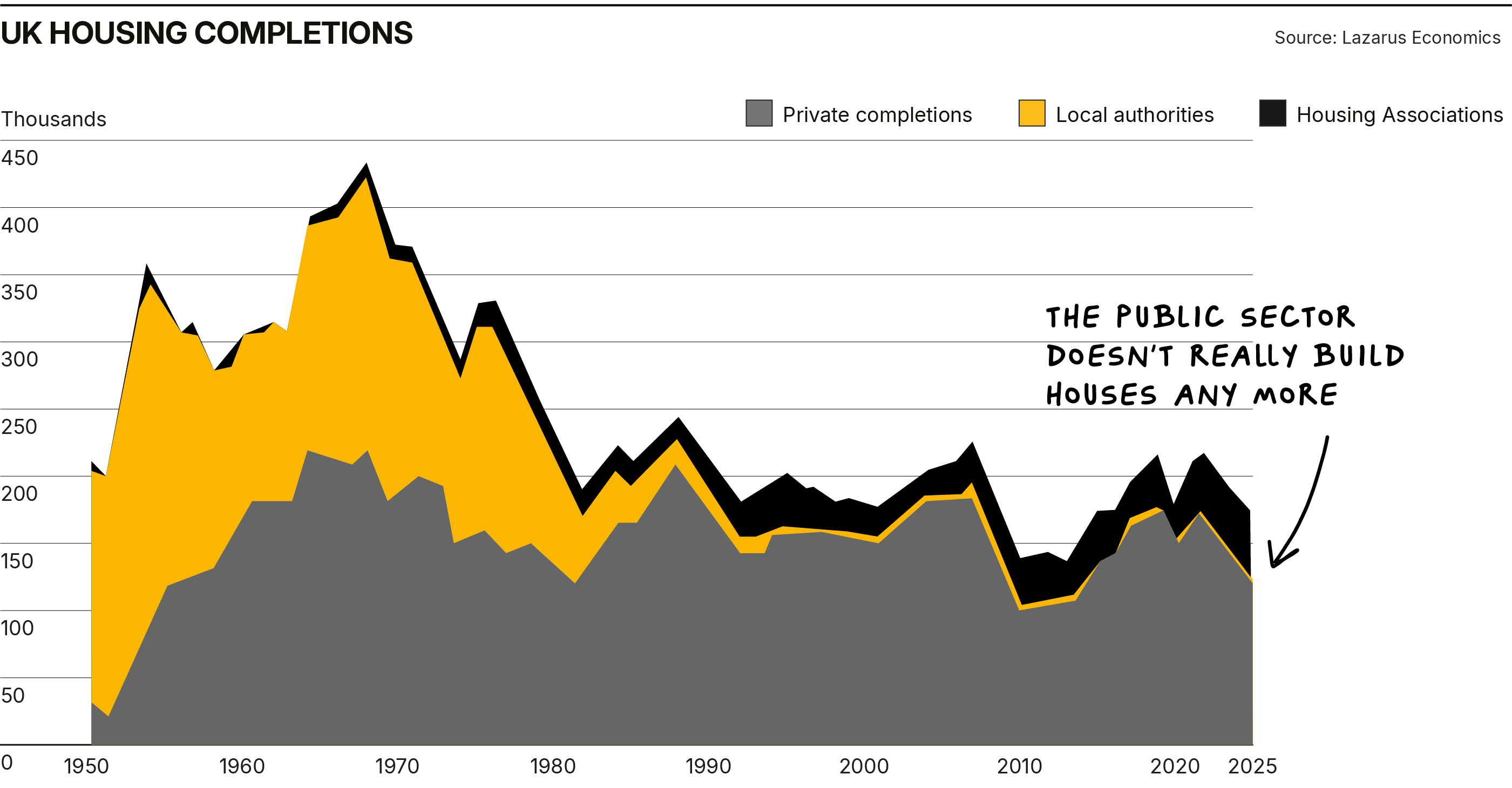

4. Perhaps the minister is unaware that the public sector doesn’t build houses anymore (its housebuilding share is barely traceable on the chart below). He also seems unaware that the affordable market, although relatively healthy, is only a quarter the size of the private sale market.

The minister cites Vistry, a volume builder now focused on the affordable market, as an example of what he is trying to promote. It partners with state-funded quangos like Homes England, under contract, to deliver (mixed tenure) rental and affordable homes alongside private sales. Unwittingly, the minister further demonstrates his ignorance by saying that Vistry (a company I know well) is “geared to long-term value creation and turnover”. As for its business model, I can assure the minister it is not focused on turnover. It’s very much focused on “achieving an industry-leading ROCE as a key priority.”

Oh dear, I thought the minister was critical of business models in the sector that were focused on “return on capital investment rather than volume”.

5. Like so many of his colleagues in government, he seems to have an appalling grasp of how private enterprise works, particularly in his home turf, the housing market. The reasons why new housing volumes are depressed have absolutely nothing to do with the muddled explanations offered up by this lifer in the public sector. Instead of pointing fingers at the sector, the minister would be better advised to look to the ludicrously arcane planning system in the UK, excessive and inappropriate regulation of the mortgage market, eye-watering levels of stamp duty, government-generated inflation that has kept interest rates high, the lack of any help for first-time buyers, and excessive and onerous regulation of the building industry (environmental, biodiversity, nutrient neutrality, building safety etc. – I am not advocating a free-for-all but much of this has gone way too far).

6. If the minister were up to the task, a good place to start might be to understand why this has happened.

That, in turn, might prompt him to address the real reasons for the low level of new housebuilding and the constipated second-hand home market.

7. Interestingly, the minister’s commentary also directly contradicts what the Chancellor and her OBR advisors believe will happen to house prices. They, rather more sensibly, suggest that prices will rise in line with average earnings. My own take is that if the MPC delivers on lower rates, then house prices may do a little better than this.

So, to conclude. Disappointingly, but not surprisingly, the housing minister, Matthew Pennycook, appears not to understand how private enterprise works—his aspirations I share regarding higher new housebuilding volumes. But the way to achieve them is not via his statist nonsense, but through reform of the mortgage market, abolition or significant reduction in stamp duty, planning reform, proper resourcing of local authority planning departments, sensible reform of building regulations, lower interest rates, and the reinstatement of schemes to assist first-time buyers.

Unless and until these come about, I am afraid, like so many other government targets, this one will be quietly forgotten about, and the minister’s new strategy will suffer a similar fate whilst rightly gathering dust on some bookshelf in Westminster.

Sometimes I read something so profoundly stupid that I have to respond. Today it was an interview in the FT with housing minister Matthew Pennycook, who was previewing yet another government housing strategy. In it, the minister reveals a staggering lack of understanding of how private enterprise works, how supply and demand operates, and what is actually wrong with the UK housing market.

Pennycook wants to encourage "alternative business models" to replace those used by the large developers, and a bigger role for the state. He thinks the current model "locks in an upward ratchet of land and house prices" and that if the government hits its 1.5 million homes target, we'll see prices level out and eventually fall. He even cites Vistry as an exemplar of his preferred approach — apparently unaware that Vistry's business model is explicitly focused on achieving industry-leading return on capital, the very thing he claims to be against.

The facts paint a very different picture to the one this career mandarin is selling. In real terms, the average house price is now below where it was twenty years ago. First-time buyer mortgage payments as a percentage of post-tax earnings are at historically reasonable levels. The public sector stopped building houses decades ago — its share is barely traceable on a chart. And housing transactions as a proportion of owner-occupiers have collapsed since the early 1990s and never recovered.

The reasons for depressed housebuilding volumes have nothing to do with flawed business models. They have everything to do with a ludicrously arcane planning system, excessive regulation of the mortgage market, eye-watering stamp duty, government-generated inflation keeping interest rates high, the absence of any help for first-time buyers, and onerous building regulations that have gone way too far. The minister would be better advised to address these rather than peddling statist nonsense about the state "leaning in" and councils "building again at scale."

Unless and until these real issues are addressed, this target — like so many others — will be quietly forgotten, and the minister's new strategy will gather dust on a bookshelf in Westminster.

Related posts

Subscribe to receive Woodford Views in your Inbox

Subscribe for insightful analysis that breaks free from mainstream narratives.