Roundup of the week: 22 August 2025

This week has been a little thin on corporate news. Still, there have been plenty of interesting developments from a UK political and macroeconomic perspective, which touch on some subjects regular readers of this update will be familiar with.

If you think I have missed something you would like to discuss, please let me know, and I will give you my view.

Watch the video version

Politics

The major events grabbing attention this week are the ongoing negotiations between Donald Trump and others aimed at securing a peace deal in Ukraine. Last weekend’s summit in Alaska between Trump and Putin kicked the process off. It has been followed by a number of important gatherings between President Zelenskyy and various European leaders, and another get-together in the Oval Office. So far, the most significant developments seem to be the offer of US security guarantees to Ukraine and speculation about a European peacekeeping force to be positioned in the country. Of course, these negotiations will ultimately depend on Russian compromise, which has so far not been evident, and so the chances of an acceptable peace deal or even a ceasefire, although improved, are by no means assured. Having said that, a sell-off in European defence companies earlier in the week and a slightly weaker oil price may be symptomatic of a slightly increased level of optimism that something positive may emerge from the frantic diplomacy that’s underway.

As the week has continued, it is becoming apparent that Russian compromise is looking less and less likely. Given that, Trump’s desire to deliver peace in Ukraine in the immediate future looks likely to fail.

Economics

UK: ONS and inflation

This week, the ONS was supposed to be producing inflation and retail sales data. Unfortunately, the retail sales numbers will be delayed for two weeks because of ongoing problems at the ONS with the quality and reliability of the data it produces. This is another example of the critical challenges confronting the UK’s statistics body. Although not yet systemically worrying, this latest failure to produce macroeconomic data reliably, accurately and on time is becoming a serious problem.

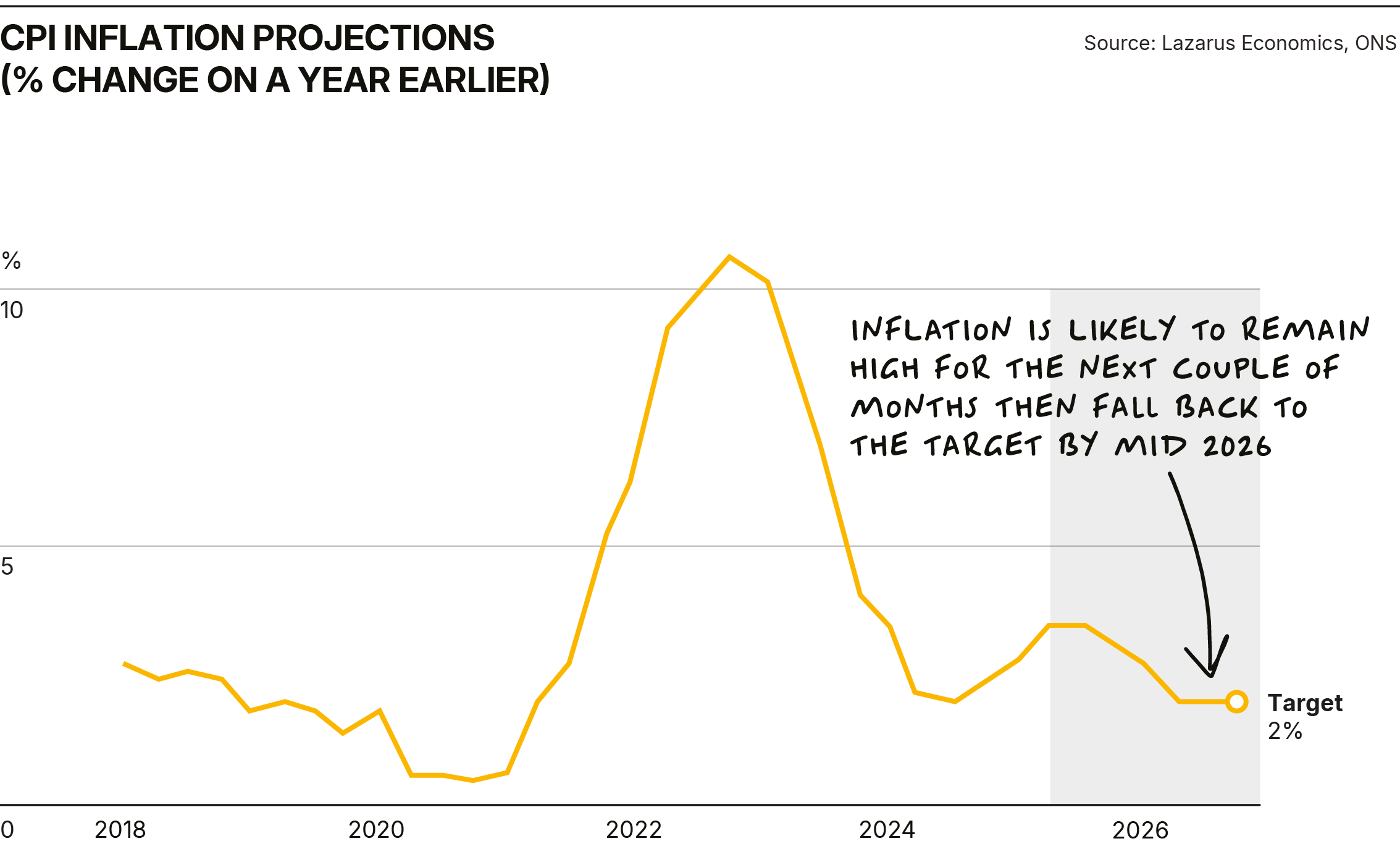

The ONS did manage to release July’s UK inflation on time. Once again, the headline number has attracted a lot of attention and the usual purveyors of doom have been busy writing a lot of negative copy about its implications for government borrowing and interest rate cuts. The reality is, as usual, somewhat different from this popular narrative.

First to the detail. The headline CPI number was 3.8% for July. In truth, this is higher than I had expected back in the spring. However, as usual, the number is still heavily influenced by base effects, the legacy of administered price increases (water, electricity, gas, bus fares, excise duty, etc) and by the additional costs levied on businesses by the Chancellor and their response to those higher costs. Having said that, the 3.8% outturn was in line with August’s Monetary Policy Report. About half the increase in overall inflation in July was due to a 30% increase in airfares, which are especially volatile at this time of year as carriers seek to maximise the seasonal travel opportunity.

Over the year to July 25, energy prices accounted for about half the increase in CPI, but food price inflation only accounted for 25bps. Looking forward, inflation is likely to remain high for the next couple of months and then start to fall fairly rapidly back to the target rate by about the mid-point of next year. Significantly for the MPC, wage inflation continues to fall, with one reliable survey pointing towards settlements consistently at 3%.

UK Stamp Duty Land Tax

Interestingly, there has been further speculation this week about what might happen to the budget in the autumn. Surprisingly, there has been some speculation about the government scrapping SDLT, and the media have jumped on this.

Unfortunately, as budgets approach, governments, in my view in error, often indulge in a sort of fiscal policy kite-flying exercise. This idea appears to be another example of that as a way of gauging a likely response. This is a mistake because the rumour is likely to kill the housing market stone dead until clarity emerges in late October or early November, or possibly earlier if the kite flying gets the thumbs down.

In fact, as I have written in recent blogs, this would be a great idea if it happened and would be just the sort of initiative that would help deliver the government’s number one priority, economic growth. It would also pay for itself many times over by catalysing more housing transactions and higher consumer spending, not just in the year the tax was abolished, but for years after. However, I suspect the government’s instincts are nowhere near as radical as this. I suspect that its predilection for creating new, or increasing existing taxes means that if SDLT were to go, some sort of other tax would take its place, albeit that the alternatives look both politically dangerous and very complicated to implement. So, I am left feeling that this rather good idea, which I have promoted as one of the best to help drive growth in the economy, will not see the light of day. I hope I am wrong!

UK Government borrowing

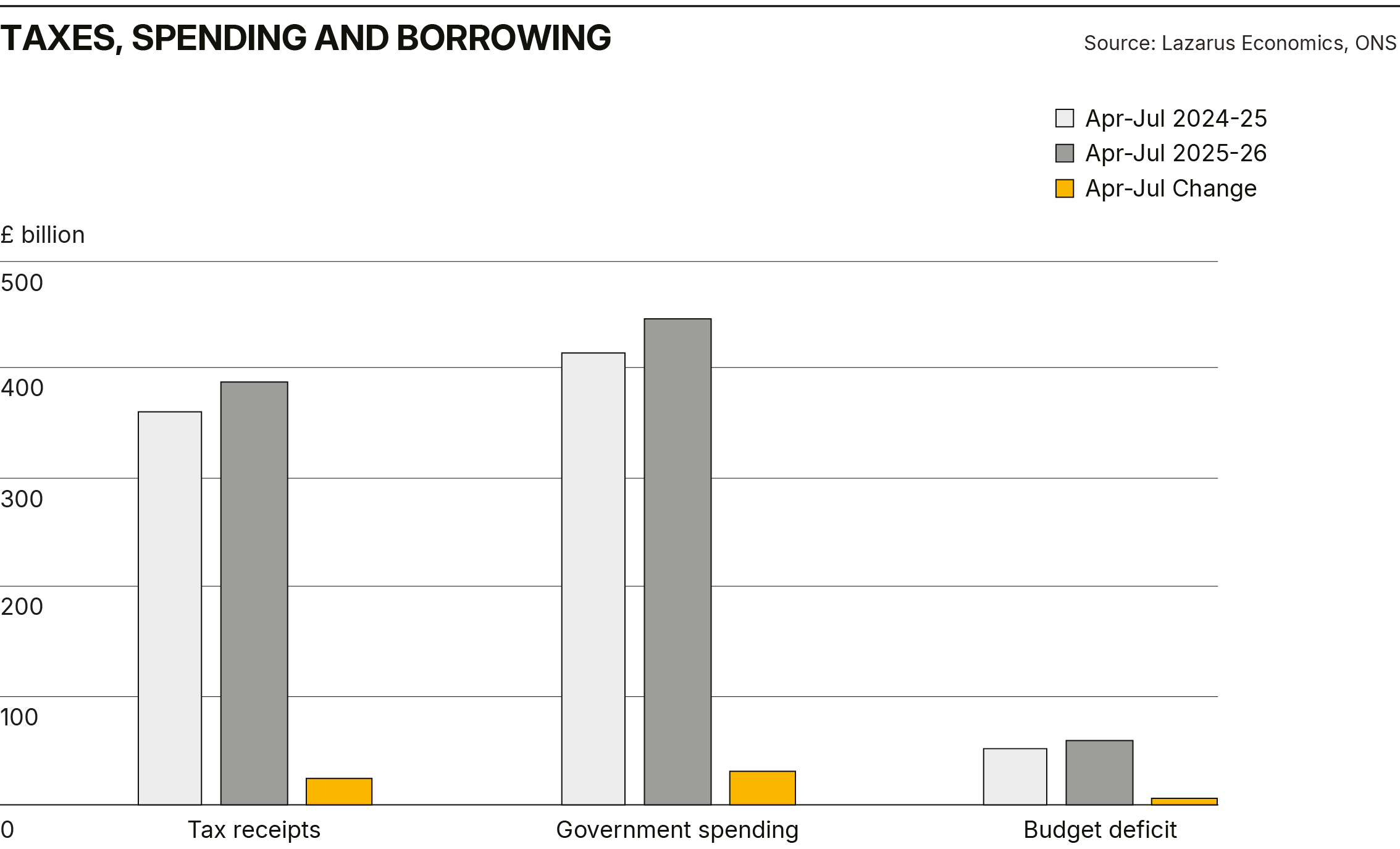

From an economic perspective, this is turning out to be a decent month for the government. Q2 GDP growth was much stronger than expected and interestingly the detail underlying the headline number was also better than the media reported. For example, domestic consumption growth was a robust 0.5% but was dragged back to 0.1% growth by an apparently big fall in net tourism, something which I am confident will be revised in time. The UK inflation data was bang in line with the Bank of England’s expectation, and today, the government borrowing data for July is also considerably better than had been expected.

In summary, the July deficit, at £1.1bn, was £2.3bn lower than a year earlier and £1.1bn lower than the OBR forecast in the Spring Statement. July is a big month for tax receipts, but contrary to the gloom and doom about fiscal black holes, the current budget was in surplus in July. For the four-month period to July, the deficit, at £60bn, was also bang in line with the OBR’s expectation.

Although government spending growth was close to a frightening 8%, it will slow towards a planned 3% growth rate over the next few months. Reflecting the recent tax changes, NI contributions were up a staggering 17.5% over the same four-month period, and tax receipts overall were up 7.25%.

Although the media has appeared to completely swallow NIESR’s gloomy fiscal black hole predictions, there is absolutely no evidence that it exists. Indeed, the government’s fiscal plans appear to be exactly on track. The “£50bn hole in the nation’s finances” only emerges if NIESR’s gloomy growth predictions come to pass. In other words, as is so often the case, underlying assumptions drive the headline narrative.

My issue is with these very gloomy growth predictions. For example, let’s take the consensus view that the UK economy will grow by 1% next year, which is close to NIESR’s downbeat expectation. Without delving into the details, I am struggling to understand how this makes sense. The UK economy will deliver close to 1.5% growth this year. Given that, I cannot see how growth will slow next year. Inflation will be lower, interest rates will be lower, there will not be the same level of tax increases, if there are any, and there won’t be a repeat of the Trump tariff uncertainty. My guess is that growth will accelerate to 2%, not decelerate to 1%.

So in summary, based on more realistic and less apocryphal growth forecast, the £50bn black hole disappears, and with it the need for further damaging tax increases.

US labour market data

US jobless claims data released on Thursday were the highest since June and added to evidence that the US labour market is continuing to cool. The data shows subdued hiring and higher unemployment. My view is that these data make it more likely that the Fed will cut rates in September, with an increasing possibility of an outsized cut.

This week’s events have quietly challenged some of the dominant narratives in markets and policy. Donald Trump’s attempt to position himself as a peacemaker in Ukraine — hosting talks with Putin, Zelenskyy and European leaders — has stirred speculation that a settlement could be closer than many expect. Markets have reacted quickly: European defence stocks sold off and oil prices edged lower, suggesting investors may be getting ahead of themselves.

At home, the UK’s inflation rate held steady at 3.8% in July, with airfares providing the biggest upward push. That came alongside rumours of possible stamp duty changes, sparking fresh uncertainty in the housing market. Meanwhile, the budget deficit in July came in smaller than forecast, adding weight to the argument that the much-discussed “fiscal black hole” might be less threatening than consensus suggests.

Taken together, these developments point to a common theme: widely accepted assumptions — whether about endless war in Ukraine, runaway inflation, or looming fiscal crisis — may not be as unshakeable as they first appear.

Watch the video version

What does all this mean for investors?

If you find these weekly updates useful, W4.0 takes you much further.

Members don’t just get the headlines explained — they see how every development connects directly to Neil Woodford’s investment strategies. Each company is chosen for a reason, and every month Neil sets out the thinking behind the changes he makes.

Inside W4.0 you’ll get:

- Transparent, research-led strategies

- Full explanations for every holding

- Monthly updates with market context

- A weekly podcast with the latest news and updates

The first four strategies are now live:

✅ All Rounder

✅ Income Booster

✅ Unstoppable Trends

✅ Top 40

Join before 31 August and get 4 months free on an annual plan (worth up to £320) — or 15% off if you prefer a monthly plan.

Related posts

Subscribe to receive Woodford Views in your Inbox

Subscribe for insightful analysis that breaks free from mainstream narratives.