Roundup of the week: 15 August 2025

Although the pace of geopolitical events remains high and the economic calendar has been busy again this week, the number of company results has diminished, thankfully, after a pretty hectic few weeks.

If you think I have missed something you would like to discuss, please let me know, and I will give you my view.

Watch the video version

Politics

Although Trump-tariff-related news has died down a little this week, we have been told of a further 90-day extension to trade and possibly wider geopolitical discussions taking place between the US and China. The mood music around the ongoing discussions remains good for the time being, and I read this week that the plan is for a Trump/Xi summit in October, possibly to sign off on a new broad trade deal. If this pans out as the rumour mill has suggested, I think this will be taken well by financial markets everywhere.

This week has also seen some potentially positive developments concerning negotiations that might bring about the end to the war in Ukraine. As always, positions are being taken ahead of a Trump /Putin summit in Alaska, with various meetings going on between President Trump, President Zelenskyy and various European leaders. However, the omens ahead of this peace initiative seem better than before the last one. Naturally, if there is a peace deal, I would expect energy prices to fall further because a deal will almost certainly include Russia getting unprohibited access to global energy markets once again. Whilst I think it would be naïve to expect a deal, the chances this time around appear better than at any stage since the war began in February 2022.

Economics

It’s been a busy week for economic releases and doom-laden stories in the British media about potential fiscal black holes.

US inflation data

One of the most important releases earlier this week concerned US inflation. In summary, the headline data was in line or a little better than had been expected, but of particular note was the fact that goods inflation was relatively muted and services inflation a little elevated. This completely confounded the consensus view that Trump’s tariffs would drive up US goods price inflation and create a major headache for the Fed, which is under political pressure to cut interest rates.

Going back to April, my view was that this lazy consensus was wrong. I said back at the start of this tariff trauma that the headline rates would end up being much lower than was first outlined in Trump’s Liberation Day announcement, (I also said a comprehensive deal with China was likely too) and also said that the lazy view that tariffs would be automatically passed on in headline price increases was wrong. My instinct was that in a competitive world where companies were fighting for market share and typically have a long-term perspective, tariff rates would be absorbed initially in profit margins. Over time, cost models would be adapted to accommodate the tariff increase. Although it is arguably too early to be completely definitive about how this plays out, the conclusion is that so far, so good.

So, the implications of this better-than-expected inflation outcome are that it is now more likely that the Fed will cut rates in September. Thus far, the market expectation is that there will be a 25bps cut, but there is growing pressure for something more substantial at the meeting, especially from the Treasury Secretary, Scott Bessent.

UK Q2 GDP data

The UK Q2 GDP print on Thursday at 0.3% was a significantly better outcome than the 0.1% expected by consensus and by the Bank of England. This is important for a number of reasons. First, the UK appears to be the fastest-growing economy in the G7 in the first half of 2025. Secondly, nominal growth at 0.8% in the quarter and 5.25% YOY is well ahead of the OBR’s Spring Statement forecast and has positive implications for the UK’s fiscal outturn this year.

Looked at from a longer-term perspective, it looks like the UK economy grew in the first six months of 2025 by about 0.5% per quarter, which is bang in line with its longer-term average and about twice the rate embedded in the doom-laden NIESR forecast that was published earlier in the week. My guess is still that the UK economy will deliver something close to 1.5% growth this year and accelerate next year to 2% growth. If I am right and given where inflation is likely to be over this period, the so-called fiscal black hole that NIESR and the media have been obsessing about this week will turn out to be non-existent. Indeed, the UK should be looking at a current budget surplus in the 2027/28 financial year, somewhat removed from the crisis fiscal view promoted by so many.

UK energy policy

Three announcements this week have once again shone a light on the increasingly bizarre UK energy policy and its central focus on net zero emissions by 2035.

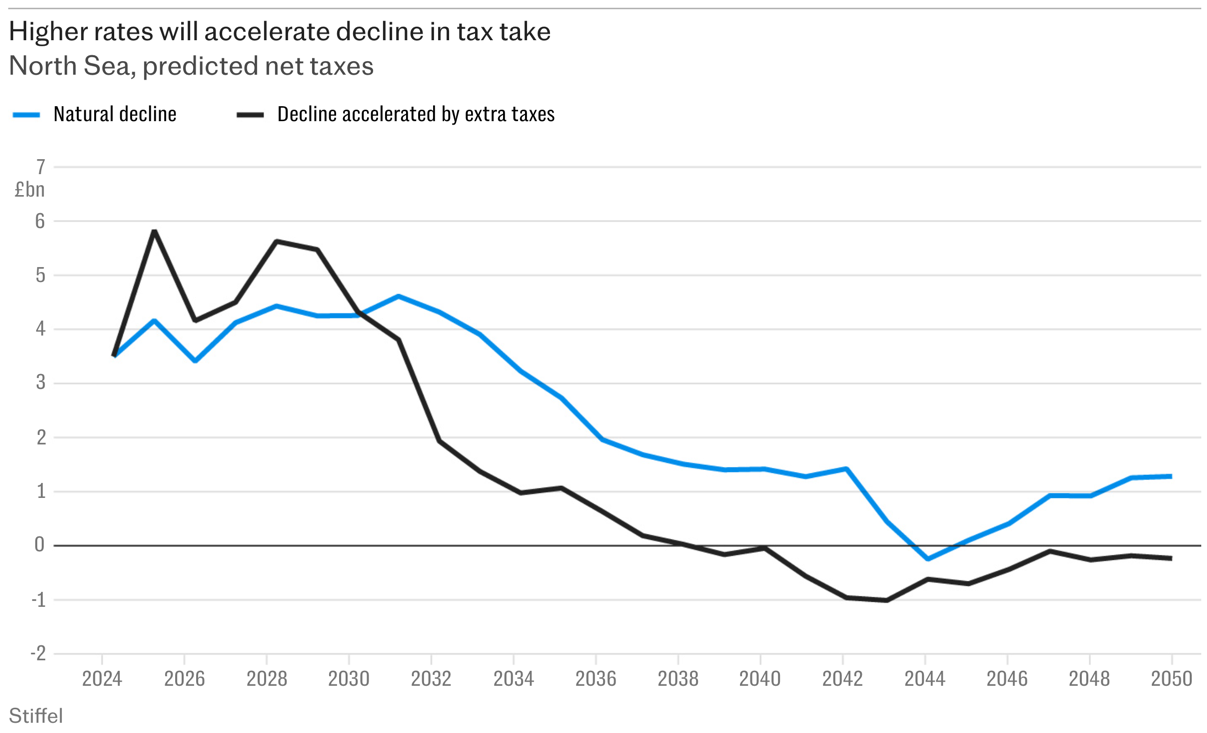

First, Harbour Energy, Britain’s biggest oil and gas producer, announced that as a result of ludicrously high costs and taxes it confronts in the UK, it will wind down its North Sea investments and instead focus on other geographies, including Norway, Argentina and possibly Mexico. This decision was announced in its interim results announcement, where it highlighted that due to the Labour government’s decision to extend the previously introduced energy profits levy to 2030, the effective tax rate on its UK operations increased from 84% last year to 111% in 2025.

Not only is this decision clearly damaging to the UK’s future energy security and balance of payments (the UK’s future imports of fossil fuels will rise), but it’s also bad news for the government, too and is yet another example of the Laffer Curve in action, as you can see in the chart below. (Higher tax rates leading to declining tax revenue)

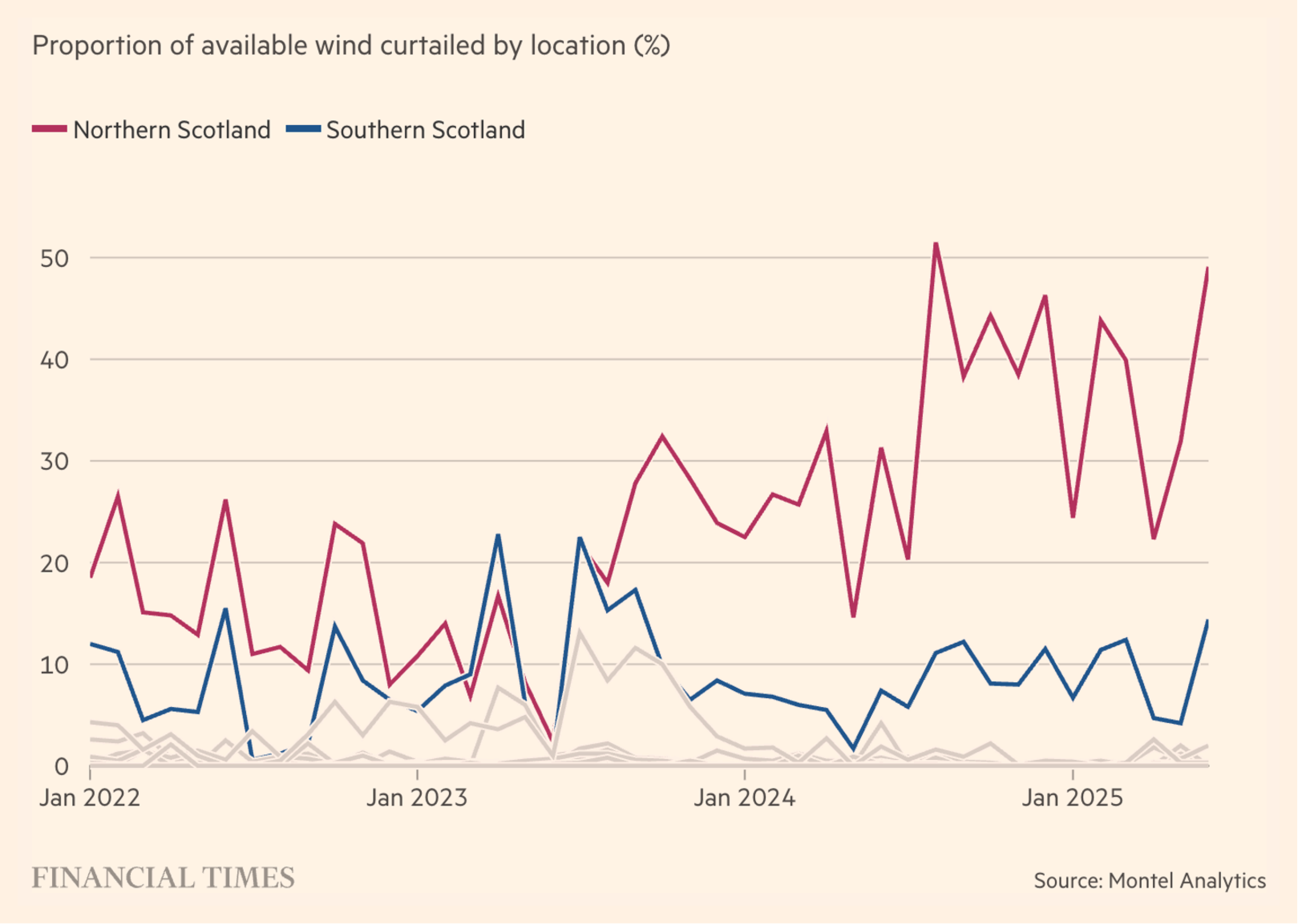

Secondly, the FT reported earlier in the week that Scottish wind farms were paid not to produce 37% of their planned output during the first six months of this year because the electricity could not be used locally or transported to where it could. This bizarre situation is a direct product of the failure of UK grid infrastructure investment to keep pace with windfarm development. It highlights the inefficiencies and hidden embedded costs of the UK’s mad dash to net zero.

The details of what is called “curtailed wind” in Northern Scotland are alarming (see below) and, according to some industry experts, are forecast to continue to grow. Frequently, because of underinvestment in grid infrastructure, the National Energy System Operator is forced to pay wind farms in remote areas to switch off whilst paying gas-fired generators in other parts of the country to fire up or increase output. You couldn’t make it up.

The third worrying story linked to the UK’s flawed energy policy was reported in the Telegraph following an interview with the boss of the UK’s largest chemical plant in Grangemouth in Scotland. The plant, which is owned and operated by Ineos, makes products used in the UK’s plastics industry and has been loss-making for several years because of very high energy prices and carbon taxes. If the situation doesn’t change soon, the plant will be forced to close, and its products will then be imported from manufacturers in other parts of the world that are not subjected to these damaging additional costs. So not only will the plant’s closure damage the local economy and the balance of payments (again), but the policies that will drive Ineos to close the plant will deliver no benefit to the environment and indeed will likely harm it given the additional energy consumed in transporting the products the UK plastics industry needs from plants in other countries.

Markets

DeepSeek

DeepSeek, perhaps China’s best-known AI business, has delayed the launch of its updated R2 model, which had originally been scheduled for release back in May. The problem appears to stem from the fact that DeepSeek was encouraged by Chinese authorities to use Huawei’s Ascend chips instead of relying on Nvidia chips as part of China’s ambition to become self-sufficient in chip technology. Apparently, the Huawei chips were not functioning well in training functions despite the presence of a Huawei team on site in DeepSeek’s offices to help with the challenges it was encountering. The solution now appears that DeepSeek has reverted to using Nvidia chips for training and Huawei chips for inference.

This episode highlights two important points: first, the non-trivial technological challenges all businesses confront in this global AI race, and second, US chip technology appears to be well ahead of China’s, a lead that the US government and US tech champions will be keen to maintain.

What to look out for next week

There are a few important economic releases that markets will pay close attention to. The first is the UK and EU inflation data on Wednesday. These series are always closely followed, especially by government bond markets, and issues tend to arise if the outcomes are significantly different from consensus. We also get retail sales data for the UK on Friday. Although this series, like so many others, can be quite volatile and affected by weather and even the timing of bank holidays, they are generally viewed as a proxy for changes in consumer confidence.

In the US, we have important labour market data on Thursday. The jobless numbers will be important because of the building consensus behind a Fed rate cut in September. If the data are strong, this will reduce the likelihood of a cut, although I still think a rate cut is odds on. If the data are weak, the pressure for a 50bps cut will increase.

This week’s data and developments have, once again, pushed back against the prevailing pessimism.

The narrative that Trump’s tariffs would fuel goods inflation in the US has not materialised—companies are absorbing costs, and inflation came in better than expected, increasing the likelihood of a September rate cut.

The UK economy also defied the consensus, with Q2 GDP growth at 0.3%—making us the fastest-growing G7 economy in the first half of the year and casting doubt on yet another round of fiscal “black hole” scaremongering.

Politically, the tone between the US and China remains constructive ahead of a potential October summit, and there’s a glimmer of hope—though far from certainty—for progress towards peace in Ukraine.

At home, UK energy policy continues to reveal its contradictions: punitive taxation driving away investment, wind farms paid to switch off, and energy-intensive industries struggling to survive.

Watch the video version

What does all this mean for investors?

If you’ve found this update useful, W4.0 gives you the complete picture.

Every week, members get the same detailed political and economic insights — but with an extra layer: how each development connects directly to our investment strategies. Every holding is there for a reason, and I explain exactly why. You’ll see the shifts I make each month, the thinking behind them, and have the chance to put your own questions to me in a members-only Q&A.

The first four strategies are now live:

✅ All Rounder

✅ Income Booster

✅ Unstoppable Trends

✅ Top 40

During August, you can get 4 months free.

Related posts

Subscribe to receive Woodford Views in your Inbox

Subscribe for insightful analysis that breaks free from mainstream narratives.