Roundup of the week: 11 July 2025

Politics

Once again, Donald Trump has dominated the political scene this week. There have been numerous further announcements on tariffs, including a delay in implementing so-called reciprocal tariffs until the 1st of August, allowing an additional three weeks for country-specific deals to be negotiated. Three country deals have also been announced with the UK, China, and Vietnam, and deals are rumoured to be close with India and the EU. However, a number of other countries, including Japan, South Korea and Indonesia, have received letters outlining steep tariff rates that will be implemented on the August deadline in the absence of progress in ongoing discussions. Brazil appears to have been called out as well by President Trump and threatened with 50% tariffs following criticism of its domestic political situation.

Interestingly, financial markets generally appear to be well conditioned to these announcements now. For example, this week, markets have been generally rising (aside from Brazil), and indeed, the UK and US equity markets are both at all-time highs.

In addition to these tariff measures (Trump has already implemented sector specific tariff rates on cars and car parts (25%) and steel (50%) from all countries) Trump also announced the intention to implement a 50% tax on all copper imports and in apparently off the cuff comments on Tuesday, a 200% levy on pharmaceuticals.

Once again, markets appeared to be pretty relaxed about these latest outbursts, presumably betting that there is a lot of hubris surrounding them and that over time, the more extreme measures will either fall away, be delayed or diluted. Nevertheless, the impact of the copper tariffs announcement has already led to a steep rise in the commodity price in the US, but falls elsewhere. As you will all now know, this is a dramatic departure from the hysteria that accompanied Trump’s original tariff announcement in early April this year.

Other political news that caught my eye this week was related to China. It appears that after some years of mounting concerns about deflation in the wider economy catalysed by excess capacity in a number of key industries, President Xi’s administration is taking steps to arrest the most intense forms of competition, Although specific policy measures have not yet been announced, the rumour machine in China is suggesting that a coordinated policy response is coming after attempts to end price wars in industries ranging from steel and solar panels to glassmaking and cars have failed to ease the deflation prevalent in the manufacturing and industrial economy. If successful, these measures would ease the troubling deflation in the economy and take some of the pressure off China’s trade relations with competitors.

Economics

Today (Friday), there are some reasonably important economic announcements which I will comment on next week, but the most interesting bits of economic news I have seen this week are the OBR’s fiscal sustainability report and the Bank of England’s Financial Stability Report.

Not surprisingly, but still depressing, is the OBR’s apocalyptic analysis, which suggests that by 2074 the UK will have a debt-to-GDP ratio of 270% and a budget deficit of over 20% of GDP on current policy settings. As usual, these kinds of forecasts rely on all sorts of conditioning assumptions similar to the ones the OBR is so keen on in its nearer-term forecasts, which have been consistently too pessimistic for years. I have not yet had time to look at the report in detail, but I question the usefulness of this type of exercise. I get its theoretical validity, but just like academic economics, these models only work when real-world things like time, inefficient markets, imperfect information, changing technology and behaviour are assumed away.

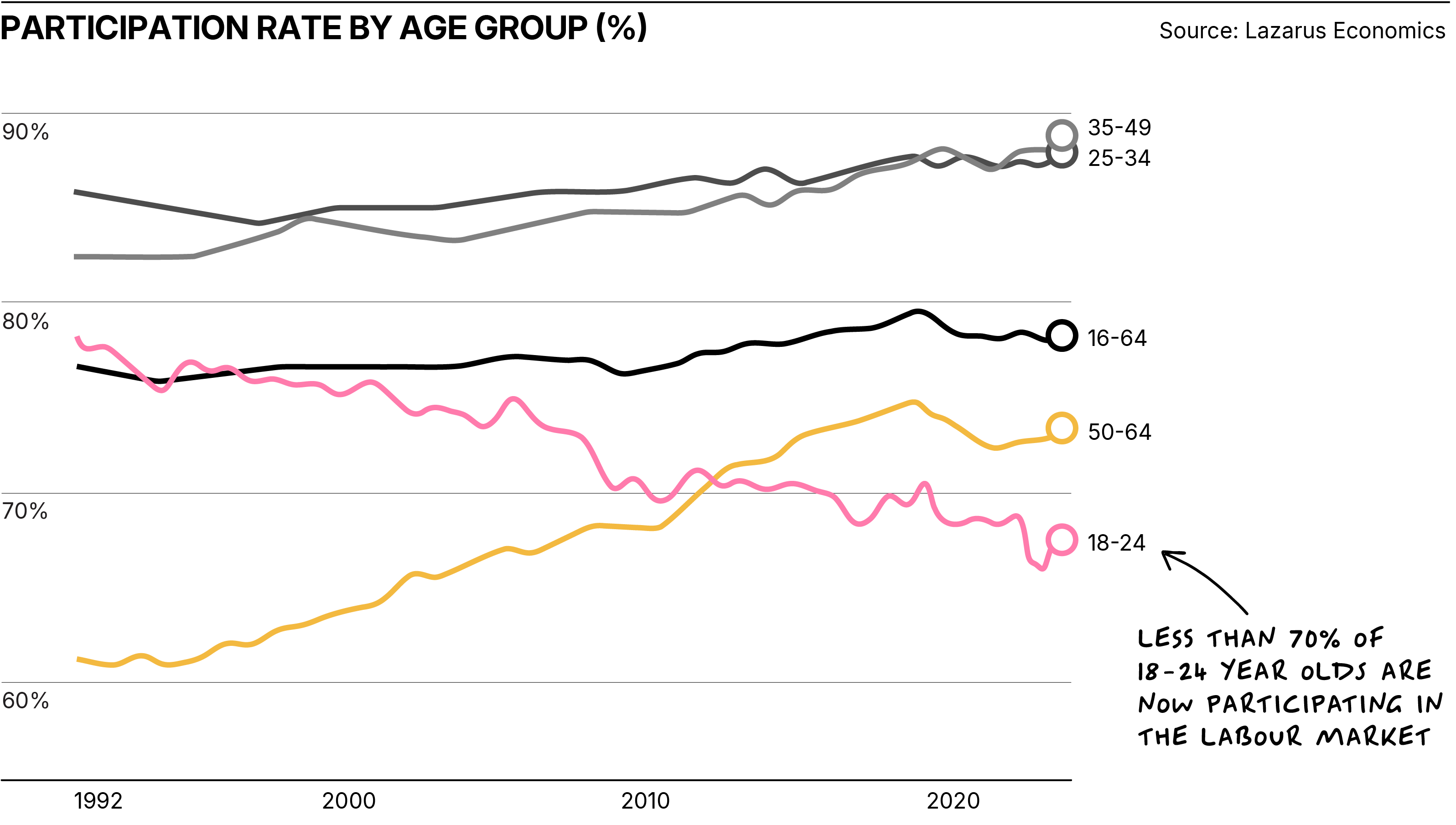

In this particular case, for example, the report draws attention to the unaffordability of the triple lock on pensions and the burden of an ageing population under current policy settings. But what is absolutely certain is that policy settings will change, as will attitudes to retirement. For example, who would have thought in 1992, that the participation rate of the oldest cohort in the workforce would increase by about 23% over the next 27 years, or for that matter, that the participation rate for those aged over 65 would nearly double to 10% over the twenty years from 1998 through to 2019. I wonder where it will be in the 2070s? (see chart below)

I also understand that the OBR hasn’t explicitly modelled the impact of AI on UK productivity in this gloom-laden report, which suggests to me that, at best, it is next to useless in helping this or any other government formulate policy for the future.

The Bank of England’s Financial Stability Report is another long report with lots of very interesting information in it. Quite how it will help the MPC make better policy decisions is not yet clear to me. However, it makes some interesting points about the mortgage market, which I will touch on in a future update. It suggests where the government and regulators might put their respective heads together to improve mortgage availability, especially for first-time buyers.

Financial markets

There has been quite a lot going on in financial markets this week, especially in relation to the W4.0 strategies. I will briefly outline the most relevant developments and aim to write more extensively about one or two of them in updates next week.

Renewable energy stocks in the US

There are a number of positions in renewable energy sectors in the Unstoppable Trends and Neil’s Top 40 strategies, and they have been heavily influenced in recent months by the dramatic changes to US energy policy instigated by Donald Trump. Initially, there was a fear that the industry would be pummelled by a combination of tariffs and the immediate policy shift away from renewables, and the sector performed very poorly as a result. More recently, those fears have abated, and the sector’s performance has improved significantly. Measures incorporated in the “One Big Beautiful Bill” were particularly relevant to this.

Initially, the fear was that US subsidies for renewable energy would end imminently, but the bill has effectively tapered the subsidy arrangements out to 2030. As a result, the near-term growth trajectory of the industry has meaningfully improved, which has been partially reflected in recovering share prices. Looking forward, I expect this improvement to continue and for the positions in the W4.0 strategies to continue to perform well as they have in recent weeks.

Memory chip companies

Earlier in the week, Samsung (not a W4.0 holding), the Korean semiconductor giant focused on memory chips, announced its second-quarter numbers. These were not very good and reflected the challenges the business is currently confronting, particularly its struggles to supply its key US customer, Nvidia, with advanced memory products.

Its challenges in getting its advanced HDM3E chips to its customers have highlighted the success of its smaller rivals, both W4.0 holdings, who are enjoying booming sales of their advanced HBM chips. Both these companies are key positions in two W4.0 strategies, and both have enjoyed a recent share price rally after concerns earlier in the year, linked to doubts about cyclical recovery in the industry and its vulnerability to tariffs, were weighing on the share prices of both companies.

Mobility solutions provider

Earlier this week, this company, a holding in three W4.0 strategies, announced its full year results to end April 2025. As is common these days, it was not immediately obvious what the underlying performance of the business was in the year, given how headline results are calculated and presented these days. However, the key points were that the business grew underlying revenues and EBITDA in line with expectations, with an especially good performance from the vehicle hire business in Spain, and this was reflected in a 2.3% increase in the full year dividend.

The outlook statement was also encouraging and highlighted the strong strategic positioning of the business in the current year. It also included guidance of mid- to upper-digit underlying EBIT growth, ahead of last year, before accounting for disposal profits. (Sales of vehicles from the fleet at prices the company doesn’t control). A slightly weaker result from disposals caused the share price to fall on the day, but this to me seemed like an odd reaction to a good underlying performance, robust guidance for the current year and a valuation that is still very depressed.

UK volume housebuilder

This business is represented in the All Rounder strategy. It issued a first-half trading update this week, which was relatively uncontroversial. It stated that the business had performed in line with expectations in the first half and added that the board was confident in the full-year outlook.

This statement was especially welcome because the company has had a series of disappointments over the last year, resulting in a steep fall in the share price in October 2024. Rehabilitation is now underway after this disappointment, and this statement was especially important in that context.

Global pharma company

This morning, this company announced a reverse profit warning, effectively guiding to a first-half outcome considerably ahead of expectations. The numbers the company is now guiding to are pretty spectacular. Revenue is now expected to be up nearly 21% in the first half, and net profit, including gains on the partial disposal of associates, is up just over 100%.

Understandably, the share price has performed very well. This company is represented in Unstoppable Trends and Neil’s Top 40.

Bonus update: Merck/Verona

Neither of these businesses are present in the W4.0 strategies, but what happened this week to both is relevant to positions in Unstoppable Trends and Neil’s Top 40. In short, Merck, a global pharma business with a dominant position in cancer therapeutics (Keytruda) confronts a very challenging patent cliff at the end of this decade and in anticipation of losing exclusivity on its biggest selling drug, and indeed the biggest selling drug in the world, is setting about building a portfolio of new, growing assets to replace the future loss of revenue.

It is looking to develop some of these internally, but some will be acquired, hence the acquisition of Verona Pharma for $10bn this week. This business has developed a key drug for COPD, which was approved by the FDA last year and has potential application across a wide range of other respiratory diseases.

Some of the biotech positions in the W4.0 strategies could follow a similar path to Verona as multiple scaled pharma businesses look to head off the challenge of the looming patent cliff by acquiring innovative, fast-growing businesses across the biotech industry.

What to look out for next week

Next week is a fairly important one for the economic calendar. Inflation data from the US is out on Tuesday, which will be watched very closely given the current very live debate about FED rate cuts. UK inflation data follows on Wednesday, which will have an important bearing on the MPC’s rate decision in early August (I still expect them to cut at this meeting). This data will be followed by important US and UK labour market data later in the week.

Given the current frequency of Trump’s tariff announcements, I am not expecting a quiet week from a political perspective. It also looks like there may be an important announcement on Russia soon. (Additional US sanctions?)

The results season has yet to get going in earnest, but we will get a trading statement from another volume UK housebuilder, which is also represented in All Rounder and Neil’s Top 40.

This week’s been packed. Trump’s back at the centre of the global narrative, announcing a flurry of tariffs — some real, some rhetorical — including a dramatic 200% levy on pharmaceuticals and threats of 50% duties on Brazilian goods. Markets barely blinked, which tells you something about how sentiment has evolved since April’s panic. Meanwhile, China looks to be gearing up for a coordinated response to industrial deflation, signalling it may finally be serious about reigning in its worst price wars.

In the UK, the OBR’s fiscal sustainability report paints a predictably dire picture — debt at 270% of GDP by 2074 — but I’m sceptical. These long-term projections rest on rigid assumptions and fail to account for structural shifts like rising workforce participation or the productivity impact of AI. Likewise, the Bank of England’s Financial Stability Report raises some good questions (particularly around mortgages), but still feels more academic than actionable.

Looking ahead, next week brings crucial inflation prints from the US and UK, a few key corporate updates, and the first W4.0 members-only Q&A.

What does all this mean for investors?

Inside W4.0, I go beyond the headlines — connecting political and economic developments to specific investment strategies. Every holding is there for a reason, and I explain why.

If you’ve found this update helpful, W4.0 gives you the full picture — including the rationale behind every position, the shifts I’m making each month, and a chance to ask questions directly in our first members-only Q&A, happening this week.

The first four strategies are now live:

✅ All Rounder

✅ Income Booster

✅ Unstoppable Trends

✅ Top 40

You’ll see every holding and the thinking behind it.

As a Woodford Views reader, you can still claim your 40% discount — but only until midnight tonight.

Related posts

Subscribe to receive Woodford Views in your Inbox

Subscribe for insightful analysis that breaks free from mainstream narratives.