Headlines, Hysteria and Hormuz

Given how quickly events are unfolding in the war in the Persian Gulf, I thought it would be appropriate to give you an update on what's happening in financial markets following the latest twists and turns.

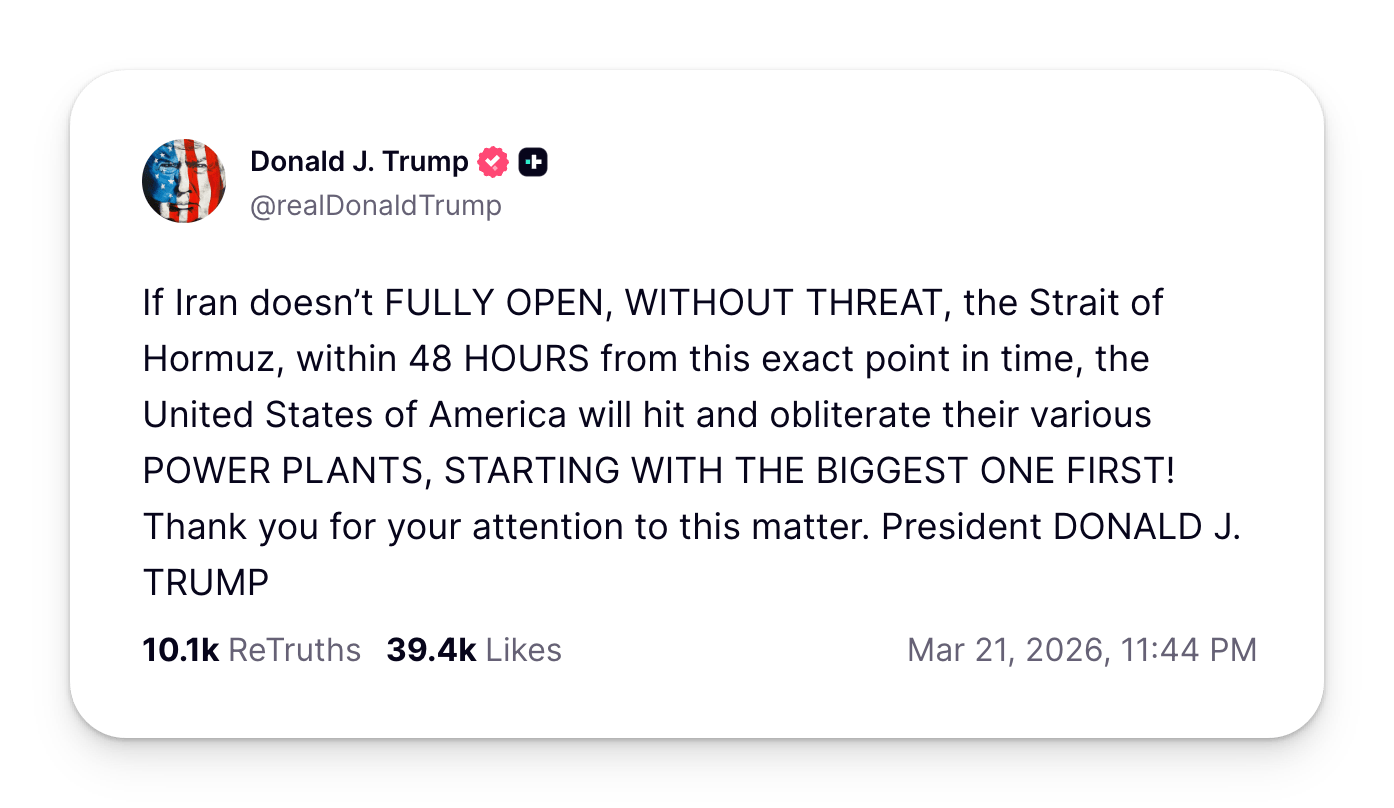

Following President Trump's warning that if the Straits of Hormuz were not open to "normal" maritime traffic soon, then the US would target Iranian civil infrastructure and power plants, financial markets started the week in a pretty black mood. Equity and government bond markets were very weak everywhere, with some big falls in Asia, along with bitcoin, gold and silver. In some respects, this sort of reaction was to be expected given that if these attacks took place, the assumption is that Iran would once again lash out at its neighbours and target key gas and oil infrastructure in the region, as it did at the end of last week.

Whilst I can understand this sort of concern, some of what I read this morning struck me as totally ludicrous and yet another example of the hysteria that all too often accompanies these events. I wish it were not so, but it seems to be an inevitable consequence of the nature of modern media and the number of commentators and journalists craving attention for their take on the situation. All too often, these lurid headlines never come to pass, but unfortunately, they can change behaviour just as they did in the months leading up to last year's budget.

This time, the prize for the most ridiculous headline must go to an article featured on Bloomberg this morning. The story concerned what was "now being priced in" by traders (people who guess a lot) in the UK money markets. In summary, the story reported that these markets had now fully priced in up to four rate rises by the Bank of England this year. Within a few hours, the story had disappeared following the latest announcement from President Trump, but the episode once again highlights not just the lack of thought and judgement by the journalist, but also the failure to understand the process which delivers this "market" view.

The money market's aggregated view this morning about UK interest rates was not the product of informed analysis or of any deep insight into the conduct of the war or its likely duration or indeed the likely policy responses to it, but in reality was the aggregation of a relatively small number of market-maker guesses driven by the latest weekend headlines about the war's escalation, the media's dark conclusions about the duration of elevated energy prices and their supposed impact on UK inflation, and finally an assumption that the automatic policy response would be to increase official interest rates.

In fact, the same goes for the oil market. Here again, the market guesses at what the price should be. The oil price is not the product of buyers and sellers of the physical commodity, but instead the product of an estimated 20–30x greater volume of financial transactions that take place in the market every day. The prices of these transactions are also the product of traders' guesses, which are heavily influenced by the latest headlines rather than being the product of thorough analysis and thoughtful conclusions. In other words, these markets, just like so many others at times like this, are driven by very short-term emotional frenzies, not by deep analytical insights. Consequently, as is evident on a day like this, they can change dramatically — literally, every five minutes.

My view, for the record, is that this war, although clearly very damaging, will not endure as others in the region have over the last fifty years. As I wrote last week, I expect this week will see moves to de-escalate and maybe, if the headlines about discussions between the US and Iran are to be believed, that is exactly what is now happening. As for interest rates, albeit that my confidence in the judgement of the MPC is low, even I could not see them making the sort of policy errors that would result in four rate rises in 2026. What they should be doing, as I pointed out in this week's podcast (watch below), is cutting rates. We will see if sense prevails.

Markets panicked on Monday after Trump threatened Iranian infrastructure. Asia sold off hard, bonds were weak, bitcoin, gold and silver all fell.

Bloomberg ran a headline claiming UK money markets had priced in four rate rises this year — pure hysteria driven by trader guesses and weekend headlines, not analysis. The story vanished within hours.

The oil price is no better — it's set by financial speculators trading 20–30x the volume of physical oil, reacting to headlines, not fundamentals. These markets move on five-minute emotional frenzies, not insight.

My view: this war won't endure like others in the region. De-escalation is already in motion. And four rate rises? Even the MPC couldn't get it that wrong. They should be cutting, as I said last week.

Related posts

Subscribe to receive Woodford Views in your Inbox

Subscribe for insightful analysis that breaks free from mainstream narratives.