.jpg)

A dose of reality

Whilst the media and the policy establishment remain so keen to leap on every piece of bad economic news, real or imagined, and ignore every positive development, I see it as my ongoing I have been particularly busy accumulating evidence that I think completely clean bowls this depressing but all too familiar economic storyline and have decided to put it down in this note. I will try to keep it as brief and punchy as possible, but given the mountain of misleading nonsense we are fed on a daily basis, there is quite a lot to say.

Let's start with the MPC and the IMF, both of which have very recently opined on the outlook for the UK economy. In both cases, unsurprisingly, the messages have been pretty depressing. At the end of April, the MPC updated its forecasts in its April monetary policy report which included three different scenarios that the committee thought could unfold in the future which to me looked like pretty bad, bad and horrendous and this happily coincided with yet another Eeyore IMF report on the outlook for the UK economy which talked about the UK economy being "especially exposed" to higher oil and gas prices. In its customary fashion, the IMF went on to say that Britain's dependence on (imported) gas meant that the looming energy shock from the Iran war would be similar to that experienced in 2022 when Russia invaded Ukraine.

And then there is the Chancellor. Every now and then, albeit increasingly infrequently, I find myself feeling sorry for politicians. The scrutiny, the criticism and the name-calling must be hard to bear at times, even for the most thick-skinned. There are also times, however, when the opprobrium is thoroughly deserved, as it was last week when Rachael Reeves decided it was a really good idea to call on supermarkets to cap prices on a range of essentials like eggs, bread and milk, and even more extraordinary, in exchange for relaxing various rules and regulations on packaging and the promotion of healthy food options. This sort of interventionist tokenism, motivated presumably by her desire to appear attuned with struggling households, betrays a complete lack of understanding of a market economy, supermarket business models and even worse, basic economics. I thought that it was especially ironic given that the supermarkets were the businesses most affected by the tax-raising and minimum wage-raising measures that the Chancellor dreamed up in her 2024 and 2025 budgets. It was these initiatives, especially on employers' NI contributions, that significantly increased costs for these businesses (Tesco is the UK's largest private sector employer with approximately 340,000 workers) and which were passed on to households through food price increases. This sort of tone-deaf politicking from someone who should know better is just the sort of nonsense that invites the criticism the Chancellor probably thinks is unfair, and further undermines trust and confidence in our ruling class.

Just by way of background, food retailers operate with 3% profit margins, and often loss lead on basic essential items like bread and milk to get shoppers through the door. I suspect that the retailers will politely tell the Chancellor to do one, which is in effect what they did last month when they declined an invitation from the Treasury to discuss how they were helping consumers. Their public response, which I thought was on point, was to suggest, in effect, that the government remove the plank from its own eye before advising the supermarkets to attend to the sawdust in its. Or, in other words, stop generating inflation through your own fiscal policy initiatives before lecturing the private sector about struggling households.

Not surprisingly, before the ink was dry on the MPC's and IMF's forecasts, in the case of the IMF they were proved to be just wrong, and in the case of the MPC, the tone of their inflation comments, those on the likely "second round" effects (of energy price increases) and explicitly, the decision of the Chief Economist, Huw Pill, to call for higher rates are already looking way too pessimistic. Equally, Reeves' embarrassing intervention coincided with much better than expected UK inflation data for April.

Quietly, and with very little fanfare, the IMF upgraded its UK growth forecast from 0.8% to 1% in 2026, less than four weeks after it was highlighting how bad everything looked for the U. In my view, this is still too low, but nevertheless, a step in the right direction. But not wishing to cut the IMF any slack, I also wanted to look at its comments about the looming energy shock in the UK and how it would be similar to that which we experienced in 2022. To do this, I thought a chart would be quite helpful, but before showing it to you, I wanted to draw attention to April's inflation data, which was released by the ONS last week.

CPI fell from 3.2% in March to 2.8% in April, which is 0.2% better than consensus had forecast. Possibly even more significant was the drop in core inflation, which fell from 3.1% to only 2.5%, reflecting, amongst other things, the significant and ongoing moderation in wage pressures in the economy. Perhaps the biggest surprise was the big fall in services inflation, but, ironically, food price inflation also fell significantly in April, down to 3% from 3.5% in March. (I wonder if Rachael has spotted this?) This good news on inflation follows hot on the heels of the better than expected Q1 GDP data, which revealed that the economy grew by 0.6% in the quarter – this is considerably more than some high-profile forecasters' expectations for annual growth in 2026 – and labour market data, which showed pay settlements in the private sector falling to 3% and a generally weaker labour market backdrop. (So, MPC, no sign of second round (inflation) effects here then.)

So just to summarise, the UK economy is growing faster than consensus thought and is experiencing lower inflation than was forecast too. Not a bad start to the year. In fact, the UK economy is the fastest-growing G7 economy in Q1, ahead, even, of the US economy. As I keep saying, this energy price shock is nowhere near that which was inflicted on the UK economy four years ago and given where household savings are right now, I believe that the UK economy will cope with this headwind far better than most forecasters believe.

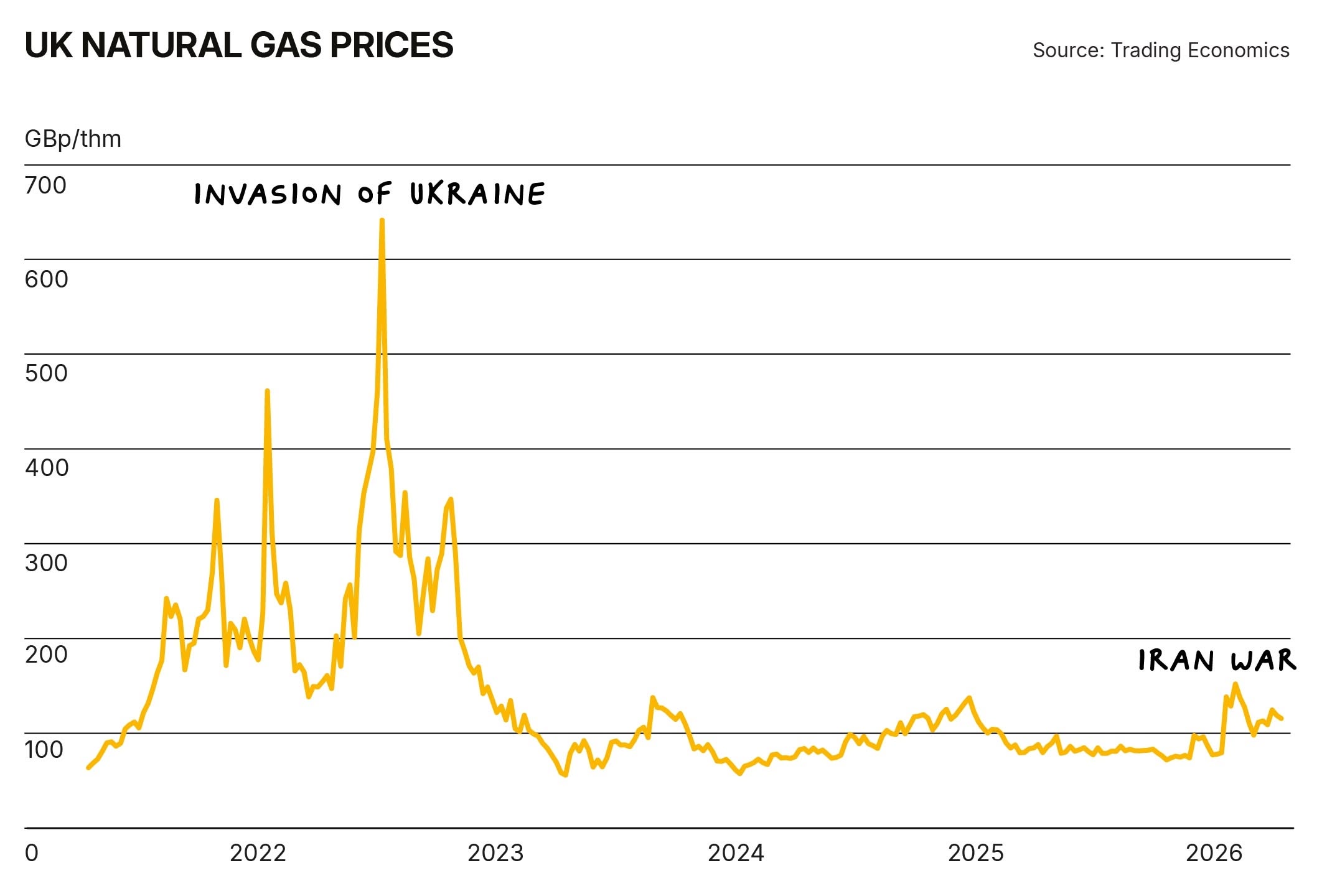

Returning to the ludicrous IMF statement about the looming energy price shock in the UK, I thought the most helpful chart would be one looking at spot gas prices in the UK over the last five years, which encompasses what happened back in 2022 and 2023 following Russia's invasion of Ukraine.

I am not sure what the IMF is looking at, but what is abundantly clear is that what's happening now could not possibly be described as "similar to that experienced in 2022". Indeed, in the latest April inflation data, UK gas prices were 13.5% below where they were a year ago, and electricity prices were 6% lower.

Before signing off on this brief myth-busting note, I thought I should also highlight the opportunity the government now has to relieve the pressure that higher fuel prices are bringing to bear on household budgets, albeit that the pressure is considerably less than the IMF was talking about a few weeks ago. This week, the PM has said that the government will postpone the 5p fuel duty increase that was due to take effect in September. Whilst recognising that this will help both households and businesses, at a cost of about £1bn, what would have been better would have been to freeze the current energy price cap until October. I estimate this would cost about £1.5bn but would save considerably more because it would not only mean a lower inflation print in September, which would reduce the indexation of billions of pensions and other welfare payments, but would also reduce the cost of index-linked debt interest payments. Sadly, it appears that this government has just walked past this opportunity to save public money whilst simultaneously helping households, but then again, why on earth would it want to do that!

Clearly there are ongoing concerns about the impact of the conflict in the Persian Gulf and energy prices but what is also clear, as I have been saying for months, is that the underlying inflationary pressures in the UK economy are easing, and especially in the labour market where private sector wage growth is now at 3%, which with 1% productivity growth, is consistent with 2% inflation which is the Bank of England's target. There are no signs of the second-round effects that policymakers are so keen to invoke when justifying their interest rate decisions. Consequently, although I still believe interest rates are too high in the UK, I do not see them increasing and believe that the MPC will remain on hold pending resolution of the US/Iran conflict, when rates can resume their downward path.

This week the consensus-doom chorus has been loud — and largely wrong. The MPC's April scenarios ranged from bad to horrendous. The IMF described the UK as "especially exposed" to an Iran-driven energy shock similar to 2022. Rachael Reeves popped up to lecture supermarkets on prices. All three deserve scrutiny.

Quietly, less than four weeks after its grim assessment, the IMF nudged its UK 2026 growth forecast up from 0.8% to 1%. Still too low in my view, but the direction matters. And the energy shock comparison is plainly nonsense — UK spot gas prices are nowhere near the 2022-23 peaks, gas prices in the April inflation print were 13.5% below a year ago, and electricity prices were 6% lower.

The April CPI data made the point more emphatically still. Headline inflation fell to 2.8% (consensus was 3%), and core inflation dropped from 3.1% to just 2.5%. Services inflation fell sharply. Food inflation moderated to 3% from 3.5%, which the Chancellor might wish to note before lecturing supermarkets on margin economics they understand far better than she does. Private sector wage settlements are at 3%; with productivity around 1%, that is consistent with the Bank's 2% inflation target. There is no second round effect, and no excuse for the MPC's chief economist to be calling for higher rates.

Add to this Q1 GDP of 0.6% — making the UK the fastest growing G7 economy in the quarter, ahead even of the US — and the doom narrative falls apart.

The government's response is characteristically half-baked. Postponing the 5p fuel duty rise at a cost of around £1bn is fine. Freezing the energy price cap would have cost about £1.5bn but saved considerably more by reducing the September inflation print and the associated indexation of pensions, welfare payments and indexed linked debt interest. They walked past it.

Rates are still too high. I do not see them rising. The MPC will hold pending resolution of the US/Iran conflict, after which the downward path resumes.

Related posts

Subscribe to receive Woodford Views in your Inbox

Subscribe for insightful analysis that breaks free from mainstream narratives.